Mechanical or operational issues with the vehicles over the course of usage.

Tide over any sudden financial requirements supplementary loans for contingencies such as tire purchase engine replacement, personal emergency.

Criteria

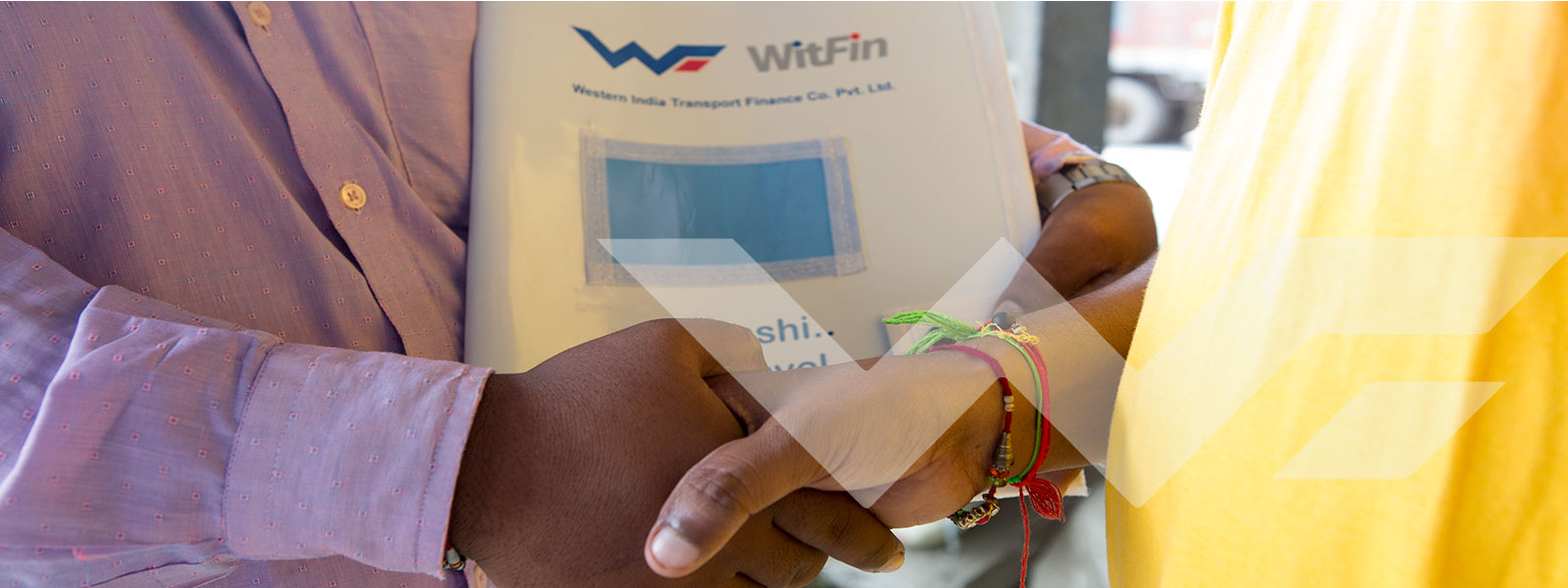

WItFin, in partnership with Accion, a global nonprofit dedicated to building a financial exclusive world, has implemented a financial awareness program which primarily provides financial education and training to build capacity of low income households to better use financial products as well as enhance livelihoods.

Beyond Credit

The Company recognizes that to achieve economic security and self-reliance, its clients require a full suite of financial services, including insurance, savings facilities, and financial literacy training. Via Accion, WitFin conducts a financial education program to enhance participants’ financial management skills and business skills. WitFin recognises the importance of having an independent organisation conduct financial education, as the Company encourages clients to value this training in and of itself towards building the capacity for prudent use of financial services. The programmes also facilitate access to appropriate products, recognising that training without product uptake and usage tends to diminish the effectiveness of the same.

Mechanical or operational issues with the vehicles over the course of usage.

Tide over any sudden financial requirements supplementary loans for contingencies such as tire purchase engine replacement, personal emergency.

Criteria

WItFin, in partnership with Accion, a global nonprofit dedicated to building a financial exclusive world, has implemented a financial awareness program which primarily provides financial education and training to build capacity of low income households to better use financial products as well as enhance livelihoods.

Beyond Credit

The Company recognizes that to achieve economic security and self-reliance, its clients require a full suite of financial services, including insurance, savings facilities, and financial literacy training. Via Accion, WitFin conducts a financial education program to enhance participants’ financial management skills and business skills. WitFin recognises the importance of having an independent organisation conduct financial education, as the Company encourages clients to value this training in and of itself towards building the capacity for prudent use of financial services. The programmes also facilitate access to appropriate products, recognising that training without product uptake and usage tends to diminish the effectiveness of the same.

We strongly value fair practice standards when dealing with individual borrowers and to serve as a part of best practice.

Applications for loans and their processing

Disbursement of loans including changes in terms and conditions

Clarification regarding Repossession

The Company shall have a built in re-possession clause in the contract/loan agreement which must be legally enforceable. To ensure transparency, the terms and conditions of the contract/loan agreement should also contain provisions regarding:

WitFin will keep personal client information strictly confidential. Client information may be disclosed to a third party subject to the following conditions:

Applications for loans and their processing

Disbursement of loans including changes in terms and conditions

Clarification regarding Repossession

The Company shall have a built in re-possession clause in the contract/loan agreement which must be legally enforceable. To ensure transparency, the terms and conditions of the contract/loan agreement should also contain provisions regarding:

WitFin will keep personal client information strictly confidential. Client information may be disclosed to a third party subject to the following conditions:

WitFin has made available facilities at each of its branches and offices for the customers to lodge and/or submit their complaints or grievances, if any.

read more...

Customers can contact us at +9122 61999 200, or email us at grievance@witfin.in or write to us at:

Grievance Redressal Officer

Western India Transport Finance Company Private Limited ("WitFin")

601A 6th Floor, Great Eastern Chambers, Sector II,

CBD Belapur, Navi Mumbai- 400703

The complaint can also be emailed at dnbs@rbi.org.in

read less...

![]() 601-A, 6th Floor, B-wing,

The Great Eastern Chambers, Sector 11,

CBD Belapur, Navi Mumbai 400614

601-A, 6th Floor, B-wing,

The Great Eastern Chambers, Sector 11,

CBD Belapur, Navi Mumbai 400614

Follow us on